New priorities transmission access reform and the future of the National Electricity Market

17 May 2023

17 May 2023

As new variable renewable energy generators enter the National Electricity Market (NEM), generators and consumers are feeling the impacts of increased congestion and increased costs. The Energy Security Board (ESB) is currently consulting on design options for a hybrid market which will assign priority access to generators, and create a new voluntary spot market called the Congestion Relief Market, or CRM.

The CRM will operate alongside the Energy Market, and the hybrid model will support and strengthen jurisdictional Renewable Energy Zone (REZ) schemes. The ESB's modelling shows it is likely to have a downward impact on the cost of capital, ultimately benefitting consumers and market participants.

The reforms aim to:

Improve investment efficiency by producing better long-term signals for market participants to locate in areas where they can provide the most benefit to consumers without increasing congestion;

Balance access and investor risk with the continued promotion of new entry into the NEM that contributes to competition and long-term consumer interests;

Remove incentives for non-cost reflective bidding and promotes better operation and dispatch outcomes; and

Create incentives for congestion relief.

Interested stakeholders are invited to make a submission or lodge any questions to the ESB by 12pm AEST, Friday 26 May 2023. For more information on making a submission, please refer to the consultation paper.

As has been the case with earlier transmission access reform proposals (such as Coordination of Generation and Transmission Investment (COGATI), the ESB's analysis appears to be based on an underlying assumption that renewable energy sites are fungible – that the key consideration is the location as it impacts the operation of the NEM.

This assumption ignores the reality that selection of sites for renewable energy projects is ultimately dictated by a range of factors, not least the quality of the resource and the environmental and community impacts. These areas are congested for a reason.

It will be difficult to incentivise projects to locate in less congested parts of the network that produce less yield or are less attractive in terms of issues that factor into site selection.

There are queries whether a COGATI-weary market will fully engage with yet another inherently complex transmission access reform proposal.

The best way forward is to tackle the underlying causes of congestion. This includes increasing the capacity and strength of the network in areas of high resource and preferred location for Variable Renewable Energy (VREs), which in part is the philosophy behind the REZ program (but attention needs to be paid at reducing the congestion at the REZ connection point by network augmentation). Although there is a capital cost involved in the network upgrades, there is a clear Low Cost of Energy (LCOE) benefit in well located VREs utilising high capacity factor and reduced environmental impacts (and reducing build costs).

The hybrid model design represents a significant departure from the existing market architecture.

Currently, the NEM open access regime allows generators to negotiate a connection to any part of the network at any time, subject only to the network connection process with the relevant transmission network service provider (TNSP) and the Australian Energy Market Operator (AEMO). Generators are then able to submit offers to sell energy into the market, which are dispatched at the volume determined by the NEM's central dispatch engine. The central dispatch engine determines the output of each generator that leads to the overall lowest cost dispatch to meet demand while maintaining system security and avoiding violations of the physical limits of the system, otherwise known as constraint equations. Generators receive the Regional Reference Price (RRP) for the supplied energy, which may fluctuate depending on load and generation.

The ESB's proposed hybrid model aims to combat the following trends in the NEM:

market participants are connecting in locations where they are not contributing new variable renewable energy and are displacing existing generation, resulting in higher costs for consumers;

lack of certainty regarding congestion and curtailment is leading to higher capital costs for investors;

market participants locating in non-REZ areas is leading to higher transmission infrastructure costs than is required; and

consumer cost is higher as more expensive combinations of resources are being dispatched to meet demand.

The two elements of the hybrid system, the priority access mechanism and the congestion relief mechanism, are discussed in more detail below.

The priority access model introduces a mechanism where generators are assigned a priority level in the market. Priority is assigned during the investment stages of a project, and given effect during dispatch once operational. The model aims to ensure that existing generators are not superseded by new generation, and incentivises new generation to locate in less congested areas. The priority access model on its own could introduce greater inefficiency, so it is necessary for priority access to be assigned in conjunction with a CRM to correct these inefficiencies.

The ESB has identified and seeks feedback on the following options to assign priority access to generators:

Queue model; or

Centrally determined tiers.

In the queue model, generators would be assigned a priority level based on the time at which the generator (or the REZ in which they are participating) reaches a defined stage in the connection process or REZ development process.

The generator's position in the queue will be automatically assigned and cannot change. If an existing generator seeks to expand their MW capacity, they would have to join the back of the queue for the expansion (but would retain their place in the queue for the existing capacity). REZs would be given a larger capacity within the queue, and would therefore be in a valuable position.

The outcome of the queue method is that a generator locating in an uncongested area will receive access more quickly, and generators will move up the queue more quickly if transmission is built to alleviate network constraints.

Under the centrally determined tiers model, priority levels called "tiers" are assigned to incoming generators by a central agency. Tiers will be delineated based on efficient hosting capacity, and assigned either through an auction process or on a first-come-first-served basis.

If tiers are determined on a first come first served basis, a generator will only move up to a higher priority tier when additional hosting capacity becomes available. If tiers are determined through an auction basis, extra space in higher priority tiers can be purchased by existing lower priority generators or new generators.

The tier model will accommodate and encourage investment in REZs by reserving capacity in a higher priority tier for the REZ.

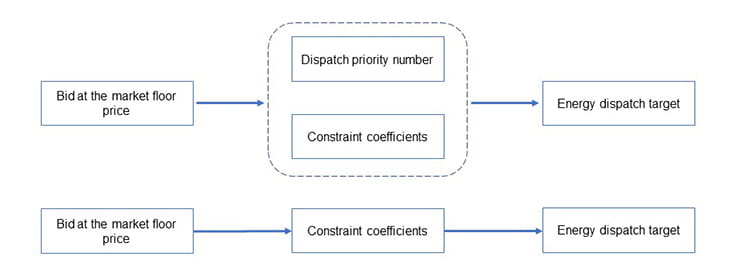

Priority dispatch under the proposed model would require changes to the algorithms used by the NEM's central dispatch engine.

One proposed alteration is to adjust the market floor price (MFP) that generators in each priority tier or queue number are permitted to bid to. For example, a generator with a higher dispatch priority could bid to a lower MFP than a generator with a lower priority, and is likely to be dispatched in preference. The generator will still receive the regional reference price for the energy supplied. However, a generator's relative priority will not be factored into dispatch where the generator bids above the MFP.

The following diagram shows how the dispatch priority number factors into dispatch calculations:

Source: Energy Security Board

The second option for implementing priority access in market dispatch is a 'sequential solve', where the dispatch is run sequentially according to the priority order. Once the highest priority solution is locked in, the dispatch process runs again moving to the next highest priority and continues until the solution balances supply and demand.

For example, if there are three dispatch priority (DP) numbers, the sequence may look as follows:

|

Dispatch 1 |

Generators with DP=1 bidding MFP |

|

Dispatch 2 |

Generators with DP= 1 or 2 bidding MFP |

|

Dispatch 3 |

All generators bidding MFP |

|

Dispatch 4 |

All generators and all bids |

The sequential solve option is likely to take longer and delay the timing of receiving dispatch instructions, and can only handle a small number of queue positions or tiers.

Both dispatch options favour a tiered, rather than queue, priority access mechanism. The ESB is seeking feedback on preferred dispatch options.

The Congestion Relief Market (CRM) design is a new voluntary spot market which aims to achieve a lower cost dispatch by encouraging more cost reflective bidding behaviours than the current Energy Market (EN) design. The CRM allows parties affected by congestion to trade with each other, so as to make the most effective use of the available grid.

The CRM design aims to:

improve dispatch efficiency by incentivising bidding behaviours that reduce system cost;

optimise the use of the transmission network; and

create market opportunities for storage and flexible demand.

The CRM will reward participants for the efficiency gains through increased profits, and will financially incentivise storage and scheduled load to charge when generating surplus power.

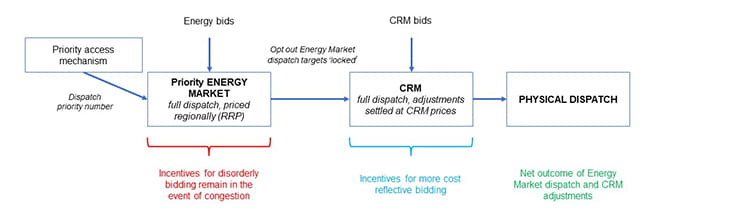

Whereas the energy market dispatch will continue to be priced at the Regional Reference Price which incentivises disorderly bidding in the event of congestion, the CRM will incentivise more cost-reflective bidding. The bidding incentives for the two markets can be visualised as follows:

Source: Energy Security Board

The CRM is a voluntary market. To participate, eligible parties must register with AEMO, else they will simply participate in the energy market. All market participants with scheduled and semi-scheduled generating units, scheduled loads and wholesale demand response units are eligible participate in the CRM. Non-market participants and non-scheduled units of market participants will be ineligible.

The ESB is seeking stakeholder feedback on key design choices concerning the following aspects of the CRM design:

a) settlement residue;

b) treatment of Market Network Service Providers (MNSPs);

c) CRM bidding structures; and

d) Frequency Control Ancillary Services (FCAS) bids and settlement.

Settlement residue is the difference between payments made to AEMO by retailers and payouts made to generators by AEMO. The CRM design must decide who receives this residue and nominate a funding source in the case of negative residues.

The ESB is seeking comments on alternative approaches to allocating CRM residue.

MNSPs are market participants that trade merchant interconnectors in the NEM. A merchant interconnector interconnects two regions, although unlike a regulated interconnector it earns revenue trading in the NEM rather than levying transmission charges.

The ESB is seeking feedback on the proposed settlement for MNSPs and whether there are any special considerations for their CRM pricing.

Given the different settlement treatment for CRM dispatch, the ESB proposes additional features for CRM bids to provide traders with more control and certainty. The two features considered are:

a) quantity limits: setting the maximum quantity that can be bought from, or sold into, the CRM in a dispatch interval; and

b) buy/sell spreads: setting a $/MWh spread between the minimum price to sell into the CRM and the maximum price to buy from the CRM.

The ESB is seeking feedback on the proposed modifications to the CRM bidding structure.

Both the energy market and CRM dispatches are complete dispatches, covering both energy and FCAS. Given the differences in design, the two dispatch runs will produce different prices for each FCAS service.

To avoid complicating bidding, only one set of FCAS bids is required in the CRM design. Thus, it is proposed that both opt-in and opt-out generators are settled on their FCAS EN dispatch outcomes and FCAS CRM dispatch outcomes are settled according to a single settlement formula.

The ESB is seeking comments on the proposed approach for FCAS bids and participation in the CRM design.

The ESB invites comments from interested parties in response to this consultation paper by 26 May 2023. The ESB will prepare final policy recommendations by mid-2023, and stakeholders will have an opportunity to make submissions on draft Rules in late 2023. The ESB has indicated that the reforms will not be implemented until late 2027 at the earliest, subject to design and technical considerations.

Please click here to see our latest Energy Alerts, as part of our Energy Alert Series or subscribe for up to date news on all things energy.

Authors: Andre Dauwalder, Counsel; Alexandria Brown, Graduate; Murray Rissik, Paralegal; and Charles Cunningham, Seasonal Clerk.

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.