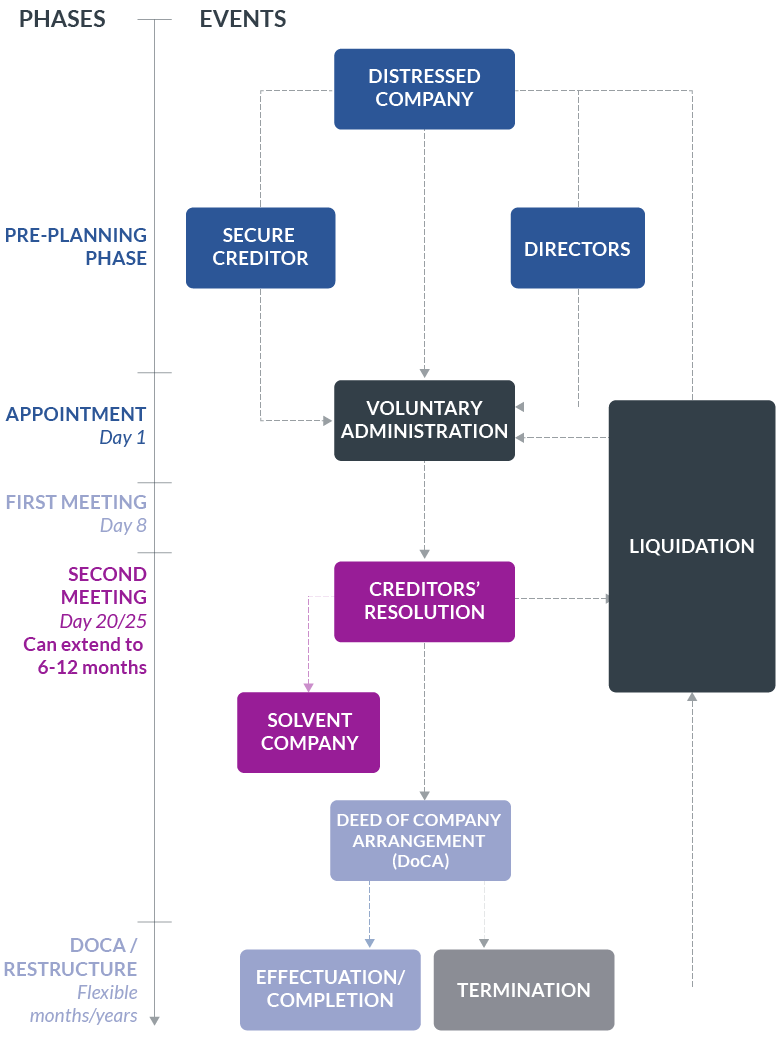

Voluntary Administration

28 October 2022

The primary objective of a VA is to maximise the chances of a company (or as much as possible of its business), being able to continue to trade. If that is not possible, the secondary objective of a VA is to achieve a better return for the company's creditors than would likely be achieved if the company had been immediately wound up.

The VA procedure:

deed of company arrangement (DoCA);

liquidation;

return of control of the company to its directors; and

and to recommend to the company's creditors which of these options is best suited to their interests.

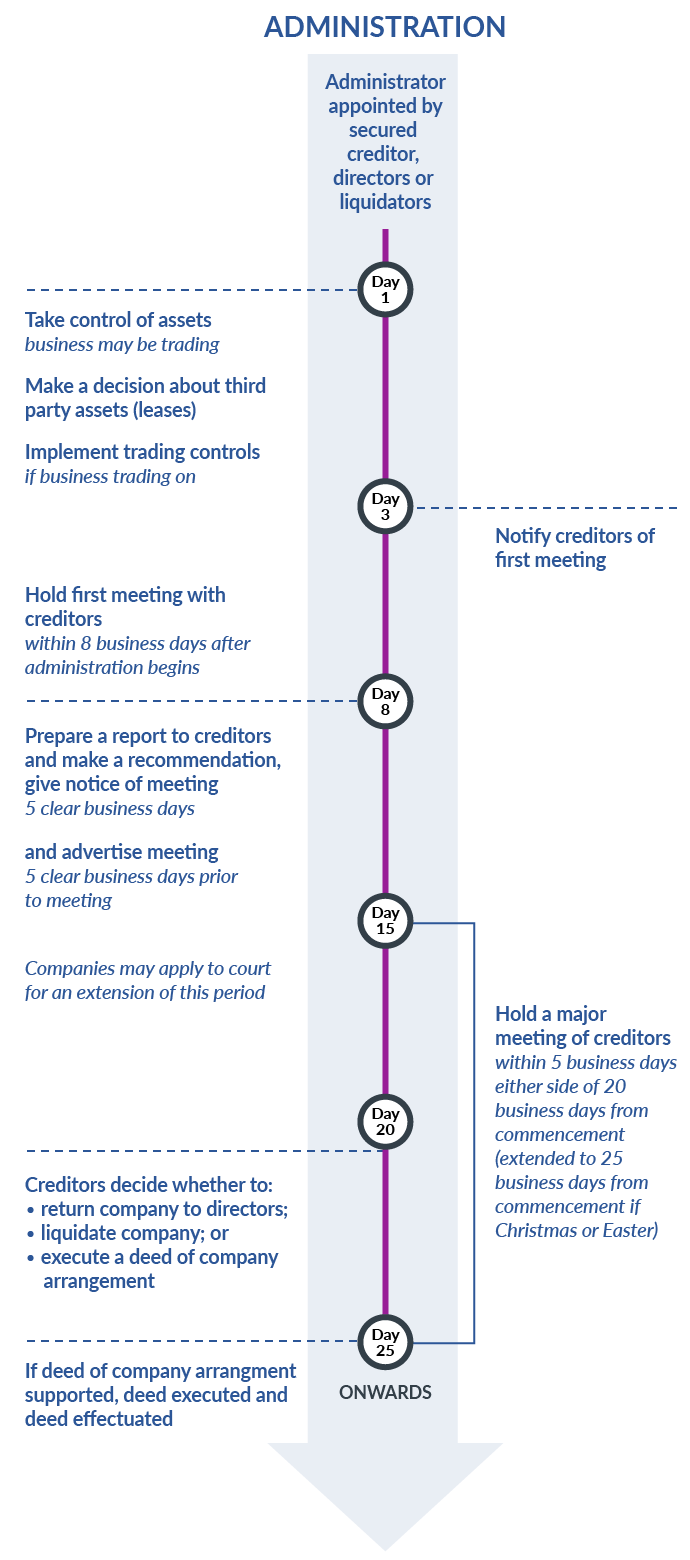

The typical timeline for the conduct of a voluntary administration is as follows:

A voluntary administrator may be appointed by any of:

In the case of a secured creditor, the option of appointing a voluntary administrator provides an alternative means to receivership (which is discussed below) of enforcing its security. It is valuable when, say, for the secured creditor to recover its debt, it assesses that it needs to sell the business of the company as a going concern and requires the protections conferred by the VA procedure to preserve the business until the sale is completed.

If liquidators identify the possibility of restructuring a company's business and maintaining it as a going concern, they can invoke the VA procedure to enable that possibility to be further assessed and for it to be considered by the company's creditors. In this context, liquidators only have the power to continue to conduct the business of a company for so long as is necessary either for its beneficial disposal or its winding up; s 477(1)(a), CA.

The administrator has plenary power to run the company's business to the exclusion of its directors. In the ordinary course it would not be expected that the administrator would sell the business or the company's assets other than as part of its usual trading activity. However, if a sale was necessary, e.g., to protect the value of that business, the administrator could sell it; Div. 3, Part 5.3A, CA.

During the course of a VA and pending a decision by its creditors as to which of the available options they wish to elect for its future, there is a moratorium on claims against the company. That moratorium applies not only to unsecured creditors such as trade creditors or the supplier of services but also to both secured creditors and the lessors of property to the company. Although, the restrictions imposed by the moratorium can be varied or lifted either with the voluntary administrator’s consent or the leave of the court; s440B(2), CA.

There are two exceptions to the moratorium:

Where the company has conducted its business outside Australia and, in particular has assets or business interests in another jurisdiction, it will be necessary to apply to the relevant court or courts to obtain orders for the recognition of the VA and its effect in that jurisdiction.

DoCAs are one of three possible outcomes of the VA procedure.

A DoCA, most often, will provide for the terms upon which the creditors of a company (but usually only its unsecured creditors) agree to compromise their claims against the company. As such, it will usually facilitate a financial restructure of a company's affairs. However, it may also provide for or facilitate an operational restructure of the company. So, it might merely provide for a continuation of the moratorium on proceeding with claims against the company thereby providing it with time to reorganise its business.

It can also provide for discriminatory treatment of creditors by which creditors with which the company wishes to continue to trade are given more favourable treatment than other creditors. For creditors who are to receive less favourable treatment, as the alternative to a DoCA, will typically be the liquidation of the company, they must receive no less favourable treatment than they could have expected to receive if the company was wound up.

For a DoCA to be approved and if a poll is demanded it must be agreed to by a majority in number representing a majority in value of the creditors attending and voting at the meeting held to consider the proposed DoCA; Insolvency Practice Rules (“IPR”) 75-115(1).

In the event of a “deadlock” (eg, there is a majority in number of creditors supporting the proposal but it is opposed by a majority in value of the creditors), the voluntary administrator has a casting vote; IPR 75-115(3). There are no strict rules which guide the exercise of that vote. Rather, administrators must vote having regard to their own assessment of the best interests of creditors.

Unlike schemes of arrangement, there is no express limitation on shareholders with claims as creditors arising from a breach by the company of its continuous disclosure obligations (“shareholder creditors”) from voting on a proposal for a DoCA. Nor is there a provision for the subordination of their claims when proving them under a DoCA (see the discussion in relation to the corresponding circumstance for schemes of arrangement).

The powers of a DoCA administrator, for the most part, will be stipulated by the deed. One important power, though, which is conferred by the Corporations Act is the power of the administrator to sell the company's shares even over the objection of the shareholders; s 444GA, CA. That is a transaction which can be sanctioned by the court. Additionally, if the company was insolvent with the result that the shareholders have no economic or commercial interest in the shares, they may be transferred without consideration. Where there is value to be gained from keeping the corporate structure, this could be a particular advantage to be gained from using the VA/DoCA procedure.

Generally, a DoCA will bind its administrator and:

In the case of unsecured creditors, the DoCA can bind those of them who enjoy preferential entitlement such as employees. However, those preferential entitlements are required to be preserved by the DoCA; s 444DA, CA.

As to both secured creditors and those creditors who are the owners or lessors of property which is in the possession of the company, they are only bound by the DoCA if they voted in favour of it; s 444D(2), CA (secured creditors) and s444D(3), CA (lessors).

However, the court, on the application of the DoCA's administrator, may restrain both secured creditors and lessors of property from exercising their rights provided that the court is satisfied that the interests of those creditors are adequately protected; s 444F, CA.

The identification of those interests involves an assessment of the interests of those creditors under their contracts with the company. This can be advantageous in the context of either a financial or operational restructure of a company because the interests to be protected are those which exist under, say, the lease between the creditor and the company. So, take the example of a lease under which the rent is $5,000 per month. It is the right to receive that rent, even if the creditor could lease the premises to another tenant for $10,000 per month, which is to be protected. So, for so long as the court is satisfied that the company can discharge its obligations to pay $5,000 per month, it can issue an order restraining the creditor from terminating the lease even if it is found there has been a breach and notwithstanding that the lessor could get a higher rent from another tenant.

As with a VA, a DoCA will not have extraterritorial effect and, accordingly, will not shield the company’s assets or other business interests in jurisdictions outside Australia unless court orders are obtained which have the effect of recognising the DoCA in those jurisdictions.

So far as the VA/DoCA option is concerned, it has a number of advantages:

(a) ease and cost of implementation;

(b) the VA automatically applies a general moratorium on actions and proceedings against the company and its property (subject to exceptions for certain secured creditors and property owners);

(c) DoCA restructuring is flexible can achieve a wide variety of outcomes, such as debt-for-equity swaps, equity transfers, balance sheet restructuring etc;

(d) approval of the DoCA only requires a majority in number representing a majority in value of the creditors who vote and the administrator has a casting vote in the event of a “deadlock”;

(e) the DoCA can discriminate between creditors without the need for separate meetings, for so long as the discrimination is not “unfairly prejudicial” in the sense that the relevant creditors would receive less than would be the case if the company was liquidated;

(f) the DoCA can be varied by a resolution passed at a meeting of creditors; and

(g) the court can terminate a DoCA.

Against those advantages:

(a) a DoCA cannot compromise or release claims against third parties, such as guarantors of the company’s liabilities, as well as against the company itself;

(b) a DoCA cannot bind a class of the company’s creditors such as, say, its lenders;

(c) a DoCA cannot bind either the secured creditors of a company or the owners and lessors of property in its possession for the purpose of accepting a compromise or arrangement of their claims; and

(d) if the company is a public listed company whose shareholders have claims as creditors because the company has breached its continuous disclosure obligations, those claims aren’t expressly subordinated to the claims of other creditors, although it has been held that the effect of s600H,CA applies to their claims with the result that they need the leave of the court to vote on a proposal for a DoCA .

A typical timeline of the DoCA implementation process is as follows:

The information provided is not intended to be a comprehensive review of all developments in the law and practice, or to cover all aspects of those referred to.

Readers should take legal advice before applying it to specific issues or transactions.